There is no fee unless we win!

EN

- EN

- ES

Imagine this: you're driving home, the light turns green, you ease into the intersection — and bam — another car slams into yours. You're shaken but alive. Now, here's the kicker: the other driver doesn’t have insurance. Or worse, they speed off, never to be found. So, who will pay for your medical bills, car repairs, lost wages, or pain and suffering?

This insult to injury happens far too often in Washington. There is a shocking number of drivers on Seattle roads and highways who have no insurance. As of 2019, Washington State had the 5th highest number of uninsured drivers in the nation at 21.7% of vehicles on the roads throughout the state.

This scenario is precisely why drivers should always purchase Uninsured Motorist coverage. Let’s break it down and explain why this coverage might be the most important part of your auto insurance policy. And remember, if you need legal guidance, contact our experienced Seattle car accident attorneys as soon as possible.

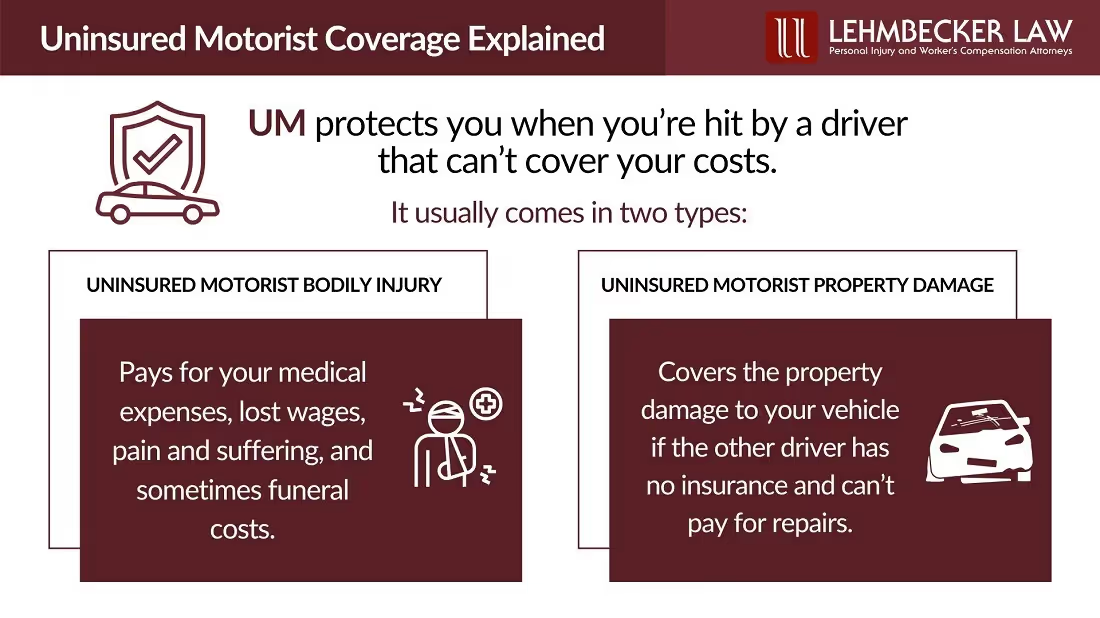

Uninsured motorist coverage (UM) protects you when you're hit by a driver who doesn’t have liability insurance. It’s like a financial safety net for situations where the at-fault driver can’t cover your costs — because they simply don’t have insurance.

UM coverage usually comes in two types:

Some states even allow UMPD to cover hit and run accidents where the driver is never identified — but not Washington. In Washington State, Uninsured Motorist Property Damage (UMPD) will only apply if the uninsured driver is identified. If the other driver flees the scene and is never found, UMPD won’t help cover the cost of your repairs.

That’s why collision coverage is essential in Washington if you want full protection for your damaged vehicle — even in a hit and run. It steps in regardless of who was at fault or whether the other driver is ever identified.

Now, let’s say the other driver does have insurance but not nearly enough coverage to pay for the damage they caused. In such cases, underinsured motorist coverage (UIM) is used to bridge the gap between the other driver's policy limits and your actual costs.

For example, if your medical bills total $75,000 and the at-fault driver's insurance only covers $25,000, UIM can step in to cover the remaining $50,000 — assuming your auto policy limits allow it.

Most people carry liability insurance because it’s required. But it’s not enough, as it only covers damage you cause to others — not what others cause to you. That’s why having UM/UIM coverage adds an extra layer of protection. Without it, you're betting your financial future on the assumption that every driver on the road has enough insurance — and that’s a losing bet in many parts of the country.

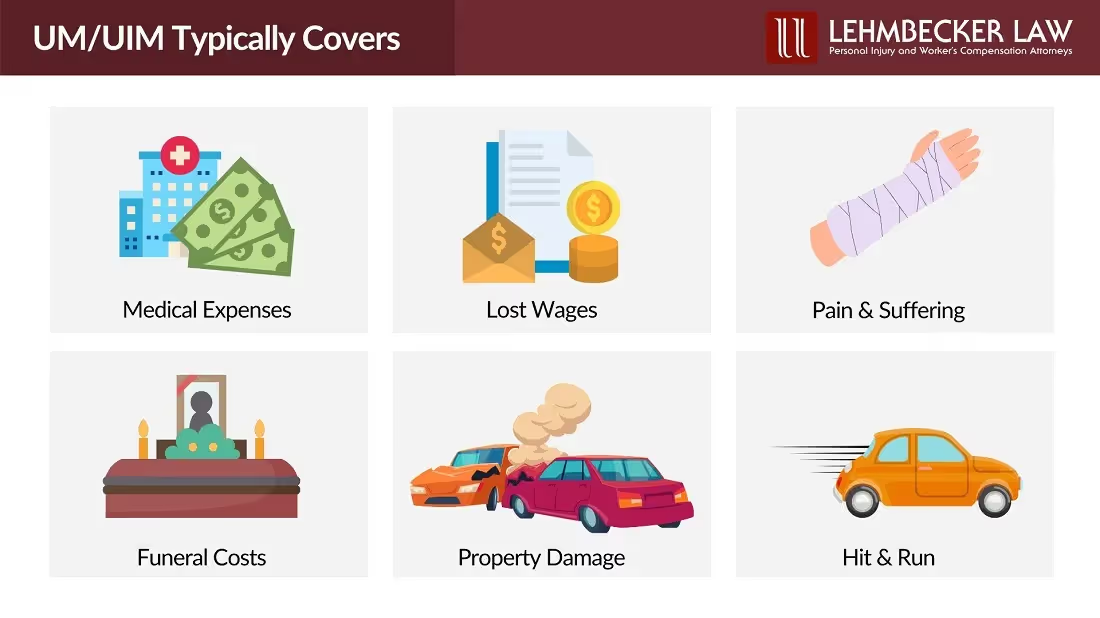

Here's a rundown of what UM/UIM can help pay for:

If you don’t have collision coverage, UMPD can be especially helpful in handling the repair costs from an uninsured or underinsured driver.

Here’s a simple rule: your UM/UIM limits should match your liability limits. If your policy offers $100,000 in bodily injury liability, you should aim for $100,000 in UMBI coverage, too. You never want to have less protection for yourself than what you offer others.

Think of it as protecting your future — your health, your job, your family’s security — from someone else’s irresponsibility.

Not quite. While health insurance might cover some medical expenses, it won’t help you with lost wages, car repairs, or pain and suffering. Plus, you might have to deal with co-pays, deductibles, and out-of-network issues.

UM/UIM coverage is designed specifically for car accidents, and it works alongside auto insurance — not as a replacement for health insurance.

In Washington, insurers must offer Uninsured Motorist Bodily Injury (UMBI) coverage, but drivers can choose to reject it in writing. Underinsured Motorist (UIM) coverage is treated the same way — it is available but optional if declined in writing.

While it’s not legally required to carry UM/UIM in Washington, it’s strongly recommended. With the number of uninsured or underinsured drivers on the road — and the reality of hit-and-run accidents — this coverage could be the only thing standing between you and a major financial headache.

If you’ve been in an accident and there’s no clear insurance coverage — either from the other driver or your own — here are three steps to take right now:

Driving without UM/UIM coverage is like high-stakes gambling at a casino. You might get lucky, or you might be left footing the bill for someone else’s mistake.

If you’re unsure whether your car insurance policy includes uninsured motorist or underinsured motorist protection, now’s the time to call your insurance provider and ask. You might be surprised how affordable peace of mind is.

At Lehmbecker Law, our Washington State car accident attorneys are committed to protecting drivers from the financial fallout of crashes involving uninsured or underinsured motorists. We’ve seen firsthand how UM/UIM coverage can make all the difference in securing compensation for medical bills, vehicle damage, and lost wages after a serious accident.

If you’ve been hit by a driver without enough insurance — or none at all — don’t try to deal with the aftermath alone. Contact us for a free case review — we serve all of Washington State.

If you’ve been in an accident with an uninsured or underinsured driver in Washington, you may still have options for compensation. Our team can help you file a UM/UIM claim and deal with the insurance company to get the coverage you need to be fully compensated.

UM covers you when the other driver has no insurance at all. UIM helps when the other driver has some insurance but not enough to cover all your damages.

Not exactly. UMPD pays for damages caused by an uninsured driver, while collision coverage applies regardless of who is at fault — but it usually comes with a deductible.

Check your auto policy documents or call your car insurance provider. It’s often listed separately from liability and collision coverages.