There is no fee unless we win!

EN

- EN

- ES

Even if you’ve never been injured in a car accident, you know the drill. You’re driving home, thinking about dinner or your next errand, when bam — someone hits your car. You pull over, shaken but okay, only to find out the other driver doesn’t have auto insurance. Now what?

Washington State drivers are especially bad at getting insured. Despite facing a $550 fine, data from the Insurance Information Institute shows that about 16.1% of Washington's drivers are uninsured. That is significantly worse than the national average of 12.6%, and it gives Washington the 10th worst rate in the nation. To protect yourself from uninsured drivers, you should consider adding the following special coverages to your own insurance.

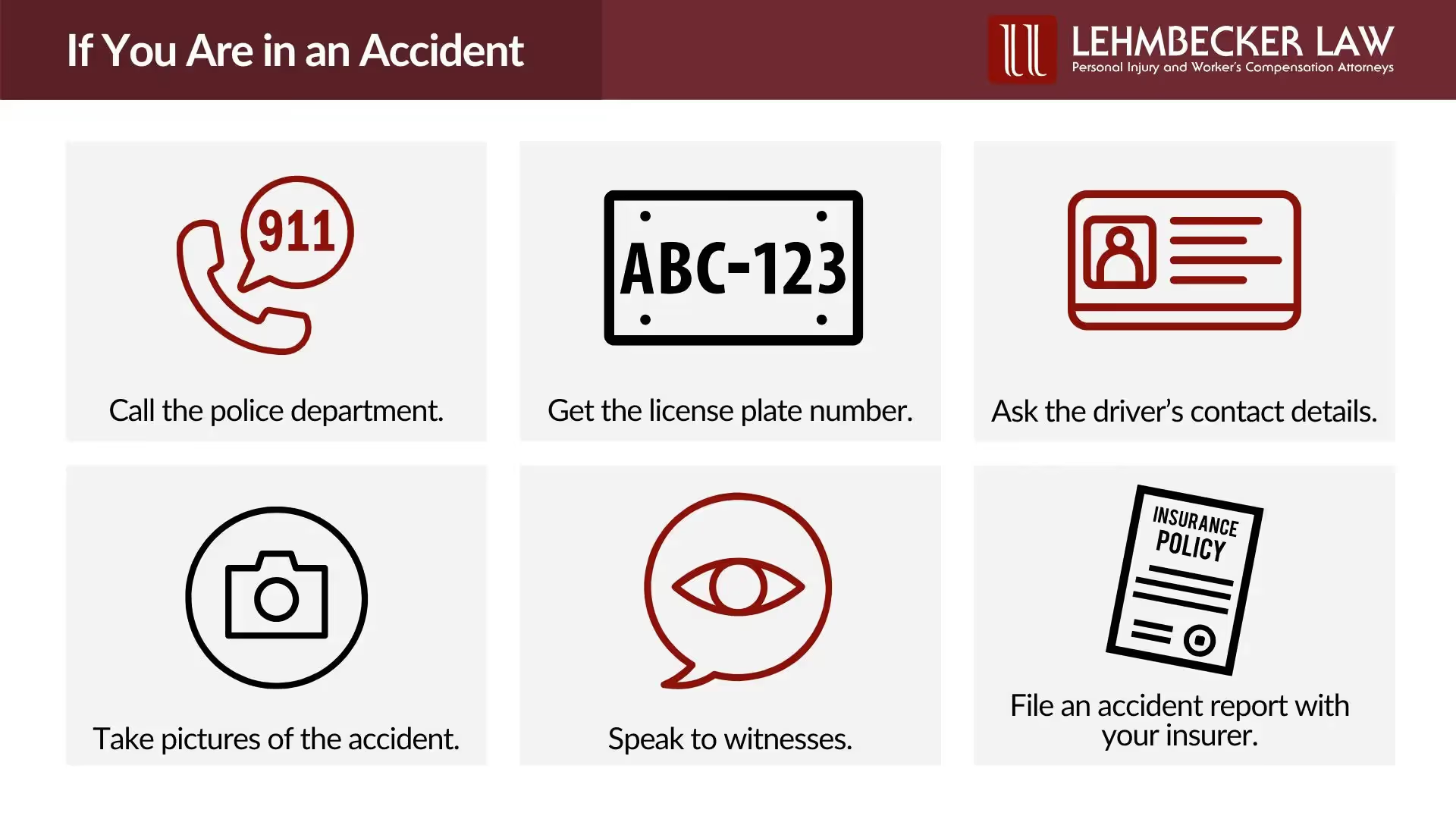

Even when the other driver is uninsured, treat the accident like any other collision. The more details you can gather, the stronger your position will be, legally and financially.

Make sure to:

This is where things get complicated, especially if the at-fault driver has no auto insurance or assets. If the at-fault driver is a student or driving with a learner’s permit, the damage may be covered by the driving school or their parents’ insurance.

If you live in a no-fault state, your own policy would pay for damages no matter who caused the crash. But Washington is an at-fault state. That means you typically file a claim against the at-fault driver, which doesn’t help much if they’re uninsured or underinsured.

Instead, you may need to rely on:

If you’ve added underinsured or uninsured motorist coverage (UM/UIM) to your car insurance policy, this coverage steps in when you’re hit by an uninsured driver. For example, if the at-fault driver has no insurance or an inadequate amount of coverage, then your own insurance company steps into the shoes of the at-fault driver to compensate the injured party.

In particular, your own insurance coverage can help if an uninsured or underinsured driver hits you and runs, or if a phantom vehicle incident occurs. In such situations, it's possible your deductible could be reduced. A phantom vehicle is one that leads to an accident, causing injury or damage, but doesn't actually make contact with your car. For instance, if another vehicle veers into your path, forcing you to swerve and crash to prevent a collision. If you plan to file an auto insurance claim for an accident caused by a phantom vehicle, you should notify the police within a 72-hour timeframe.

If you don’t have uninsured motorist coverage or underinsured motorist coverage, and the other driver can’t pay, you may be left paying out of pocket for the repairs to your vehicle, emergency medical care, long-term expenses related to injuries, or you'll have to rely on any other coverage you might have.

In this case, a car accident lawyer can help you understand how to proceed, including exploring court options or negotiating with your insurance company.

If your policy includes collision coverage, it can help cover the costs of repairing or replacing your car, even if the uninsured driver was at fault.

Personal Injury Protection (PIP) coverage pays for your medical expenses and wage loss incurred from motor vehicle injuries, regardless of who is at fault. Thus, even if the other driver is uninsured, or the accident was your fault, you will have compensation for at least $10,000 in medical bills (you can also pay for higher coverage, typically $35,000). This medical insurance is superior to most private insurance. There are no deductibles or co-pays. There are no arbitrary limits on provider visits (like chiropractic or physical therapy visits), and you can see any physician you choose. PIP coverage is a great value and is highly recommended.

After any car accident, you should call the police so that a report can be filed and get immediate medical treatment if needed. Try to record the other vehicle's license plate number. Then try to get full contact information from both the other driver and any witnesses. Document all your costs in the coming days, including items like medical care and a rental car.

If you don't have uninsured motorist coverage, collision insurance, or personal injury protection on your policy, you'll need to pay for repairs, medical bills (unless you have health insurance), and maybe a rental car. You may then personally pursue the at-fault party directly to recover your costs.

If an uninsured driver fails to pay collision damages, you may report it to the WA State Dept. of Licensing (DOL) by completing a Motor Vehicle Claim for Damages within 180 days of the collision.

Since it can be difficult to collect from an uninsured driver, it's best to make sure you have UM coverage under your own insurance. And if you're struck by an uninsured driver, get legal help at once to maximize your ability to recover all compensation to which you're entitled.

If the at-fault driver was a minor using a family-owned vehicle, you may also have a case under Washington’s Family Car Doctrine, which holds parents financially responsible for negligent driving by their children. This could give you an additional route to pursue compensation if your own uninsured motorist coverage isn’t enough to cover your losses.

Yes, you can file a personal injury claim against the uninsured at-fault driver. But here’s the issue: people without insurance often don’t have the financial resources to pay a court judgment. So, while legal action is possible, recovering compensation this way isn’t always effective unless the person has significant assets or income.

That’s why it’s often more practical to work through your insurance provider first and consult a personal injury lawyer to explore your options.

Being hit by an uninsured or underinsured driver can leave you feeling helpless, especially when you're already dealing with pain, stress, and mounting bills. At Lehmbecker Law, our Seattle car accident attorneys understand the frustration of these situations, and we’re here to help.

We’ll review your insurance policy, investigate the accident, and fight to recover compensation, whether it’s through your insurer or by holding the at-fault driver legally accountable. Our goal is simple: to protect your rights and help you get your life back.

Contact us today for a free case evaluation. We’ll handle the legal side so you can focus on healing.

Don’t let someone else’s lack of insurance ruin your recovery. Lehmbecker Law is ready to help.